How does the compensation scheme work?

From calculation to settlement

Have you made use of a revolving consumer credit facility with a variable interest rate at any time since 2001? If so, you may have paid too much interest. If that is the case, you will be compensated. Below we explain how we calculate this compensation and how you will be compensated.

Important message: compensation scheme is being adjusted

We are adjusting our compensation scheme for revolving consumer credit. If you qualify you will now also receive compensation for compound interest (interest on interest). This was decided following a ruling by the Appeals Board of the Dutch financial services complaints authority (Kifid) on 10 August 2022. If you have yet to receive your personal offer you will receive a proposal that includes compound interest. If you have already accepted your personal offer and you qualify for additional payment you will be contacted automatically.

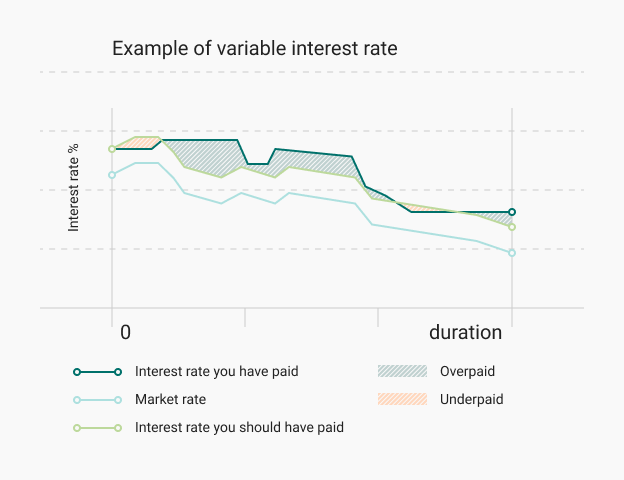

How do we calculate your compensation?

- Movements in your loan's interest rate

When did your interest rate go up or down, and by how much? - Movements in market rates for comparable products

How much did the market rate rise and fall in the same period? - The movements that there should have been in your interest rate

Were the movements in the interest rate for your loan sufficiently in line with the market rate for comparable products? - How much interest you should have paid

If your interest rate had moved in line with market rates, how much interest would you have paid each month? - The amount of overpaid interest

What is the difference between the amount of interest you paid and the amount you would have paid if your interest rate had moved in line with the market rate? We calculate the amount of overpaid (or underpaid) interest for each month. We then add the monthly amounts up (or deduct them in the case of underpayment) to work out the amount of compensation. Important! We may have previously reached agreement on adjusting your loan. In that case, the benefits you received as a result may be deducted from your compensation. - We then increase your compensation by adding a 5% markup.

Important information about the calculation

More about the calculation

- Have you previously received money from us, such as any compensation, reduction and/or cancellation of your debt? If so, we will deduct the relevant amounts from the compensation.

- Did we ever lower your interest rate or convert a revolving credit facility into a service loan with a lower interest rate? In that case, your interest rate may have temporarily been lower than it should have been based on the market rate. As a result, your compensation may be lower.

- Did you obtain a payment holiday during the coronavirus pandemic? If so, that period will not be included in our calculation of the interest you paid, as you did not pay any interest during the payment holiday.

- If you would like a more detailed calculation of the amount of compensation, please contact us by phone.

More about the interest rate

- The market rate used in our calculation is the market rate used by the Dutch Institute for Financial Disputes (Klachteninstituut Financiële Dienstverlening (Kifid). In the case of the Flexibel Krediet facility and the revolving credit facilities provided by ALFAM and ICS, the market rate is based on data from the Dutch Central Bank (DNB) and Statistics Netherlands (CBS). It is possible that a different market rate could be used for the Flexibel Hypotheek Krediet facility. Kifid is still dealing with legal proceedings relating to this product. With respect to this product, we will follow Kifid's ruling.

- The interest you should have paid is not the market rate for similar products as used by us in the calculation. We use this market rate solely to analyse when the rate rose or fell. Your interest rate should have followed these movements. ABN AMRO sets the interest rate for every credit product. When setting the interest rate, it considers factors such as the price of money on the market, risk costs, operating costs and profit. The interest rate charged by ABN AMRO can therefore be higher or lower than the market rate.

What start date is used to calculate the compensation?

For the purpose of calculating compensation, we use 2001 as the start date unless you took out your loan at a later date, in which case the start date is the date on which your loan came into effect.

If you currently have an outstanding balance, we will calculate the compensation up to the date on which we set a new interest rate for your loan under this scheme. It may be that the interest you currently pay does not yet follow the market rate. In that case, we will adjust the interest rate in the near future. We calculate your compensation from the start date up to the date on which we adjusted your interest rate.

Why was 2001 selected as the start date?

In consultation with the Dutch Consumers’ Association, we had initially opted for a workable compensation approach starting 1 January 2008. This way, we could quickly compensate a large group by digital means. Various investigations in recent months have shown us that client data from the period before 2008 can also be retrieved or reconstructed, with some additional effort. We have therefore decided to offer compensation from 2001 onwards where possible. Where we do not have the complete data, we will do our best to make a good estimate. Where we do not have any data at all, we cannot make an estimate and therefore cannot offer compensation.

How will you be compensated?

Is the amount of compensation equal to or greater than € 50?

If the compensation comes to € 50 or more after deduction of any previous benefits you received, you will be compensated as follows:

- Do you have any arrears? In that case, your compensation will first be used to reduce your arrears.

- Does your revolving credit still have an outstanding balance? In that case, your compensation will be used to reduce this balance.

- Is there sufficient compensation to repay your outstanding balance in full? In that case, we will transfer the remainder to you.

- Do you currently not have an outstanding balance at this time? In that case, the full amount of your compensation will be transferred to you.

This will be done no later than ten working days after you agree to our offer.

Does your compensation amount to less than € 50?

If your compensation amounts to less than € 50, the interest you paid moved almost entirely in line with the market rate. In consultation with the Dutch consumers' association (Consumentenbond), it has been decided that €50 is a reasonable threshold for compensation.

Important information

By accepting the offer, you grant us full and final discharge. This means that you can no longer file a complaint or start legal proceedings relating to the interest you paid on the relevant product.

Why does your compensation take the form of a reduction in your outstanding debt?

All credit must eventually be repaid. We believe it is important that you do not use your credit facility for any longer than you need to. Using the compensation to reduce your outstanding debt is in keeping with this guiding principle. If you require more financial leeway, you can apply for a loan again. We will then assess your application on the basis of your current situation.