The new EU tax disclosure rule DAC6

Has your internal group financing structure been amended? Have you completed a cross-border merger within the group? Has an entity that’s located in an EU-blacklisted country been added to the group’s cash pool? Have you converted an intra-group loan into equity?

What is DAC6 and why should I care?

DAC6 is an EU directive that requires member states to impose compulsory reporting obligations on intermediaries and taxpayers in relation to potentially aggressive cross-border tax arrangements. That is, arrangements that meet one or more pre-defined hallmarks. Local EU tax authorities will exchange reported DAC6 arrangements with the tax authorities of all other EU member states.

The fact that an arrangement is reportable does not mean, or even necessarily imply, tax avoidance. However, failure to comply with DAC6 could mean significant sanctions under local law in EU countries. In the Netherlands, for example, non-reporting could result in a fine of up to EUR 870,000 - for each case.

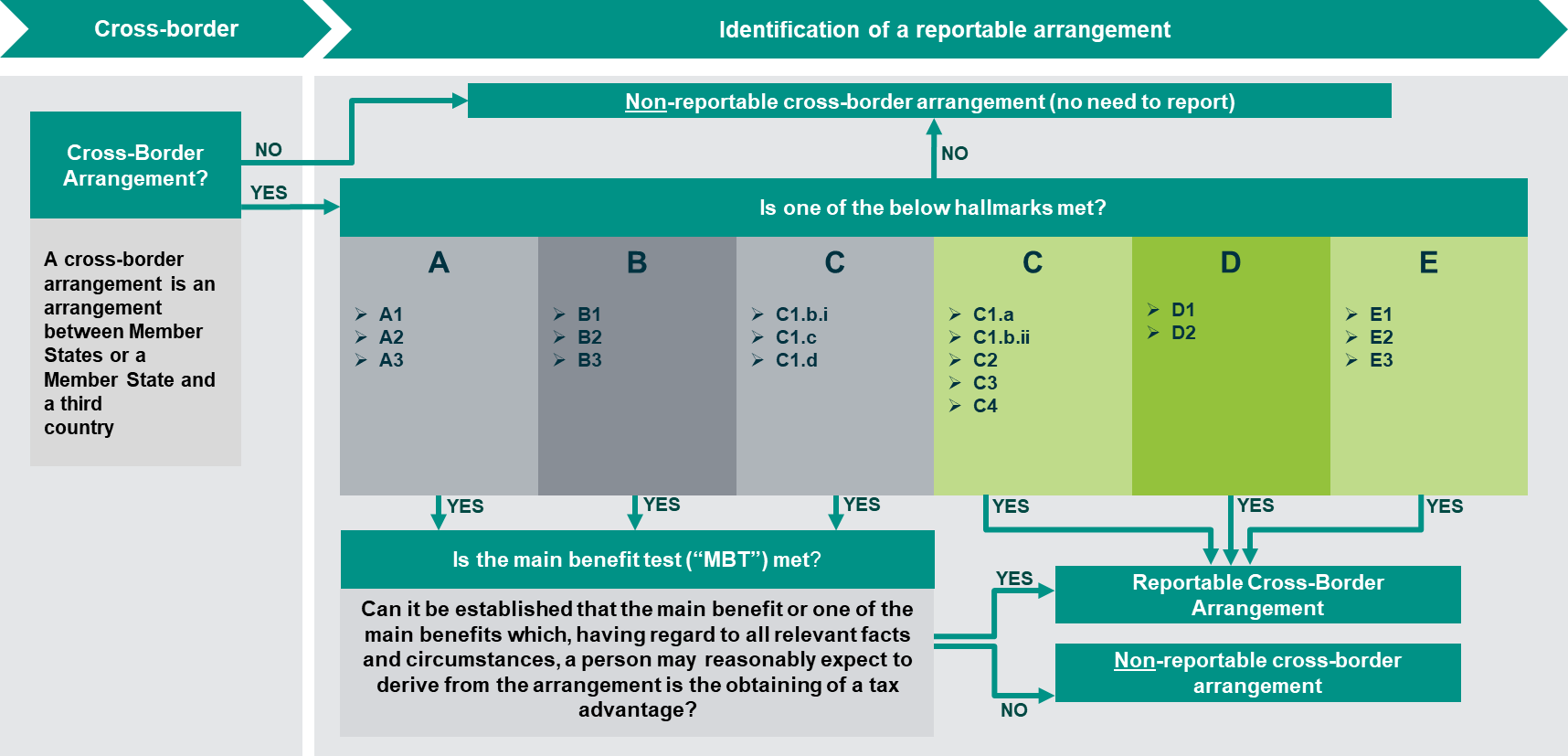

Identifying a reportable cross-border arrangement

The flowchart below provides an overview of how to identify a reportable cross-border arrangement (RCBA):

- there is an arrangement with a cross-border element (and a link to the EU);

- that arrangement meets one of the hallmarks;

- and (where relevant) the main benefit test is met.

It’s worth noting an arrangement is a very broad concept. It also includes a series of arrangements, and any one arrangement may also compromise more than one step.

The hallmarks are characteristics or features of cross-border arrangements that carry a risk of tax avoidance, and are divided into five categories. The scope of the hallmarks, particularly those not subject to the main benefit test, is very wide.

Category A: generic hallmarks, such as an arrangement where intermediaries are entitled to a fee, based on the tax benefit obtained by the taxpayer; or ‘standardised’ arrangements that can be easily marketed by intermediaries.

Category B: arrangements that contain certain tax planning features, such as the conversion of income into another category of lower-taxed income.

Category C: arrangements related to cross-border payments between related entities, such as deductible payments made to entities in low-tax jurisdictions.

Category D: arrangements concerning reporting obligations, such as arrangements that undermine information about beneficial owners.

Category E: arrangements concerning transfer pricing, such as the cross-border transfer of assets resulting in a taxpayer having a substantially lower EBIT.

To be reportable, one or more of the hallmarks must apply. But some hallmarks only apply when they fulfil the main benefit test. That is, if it can be established that the main benefit or one of the main benefits -a person may reasonably expect to derive from an arrangement- is the obtaining of a tax advantage.

Who is responsible for disclosing an RCBA?

Intermediaries with nexus in the EU have primary responsibility for disclosing relevant transactions to the corresponding jurisdictions.

But note, intermediaries aren’t just those providing tax advice. Anyone who facilitates the implementation of an arrangement that meets one of the hallmarks -regardless of the kind of advice, aid or assistance they provide- may be an intermediary. So not just tax advisors but also, for example, law firms or banks.

Where no intermediary is involved, or the intermediary opts to use their legal privilege (e.g. a law firm), the obligation to report then shifts to the relevant taxpayer themselves.

Timetable

The DAC6 reporting obligation applies to RCBAs implemented on or after 25 June 2018. The original reporting obligation start date was 1 July, 2020. However, following the Covid-19 pandemic, many EU member states have postponed this to 1 January 2021. As from 1 January 2021, RCBAs need to be disclosed within 30 days of any advice being given or implementation of the arrangement being started.

This article discusses the main rules that follow from the DAC6 directive. However, it’s important to bear in mind that DAC6 will be implemented differently and with local variations across EU member states.