Cryptocurrencies part 3: tokenisation

The technology, tokenisation and digital currency

The Economic Value of Distributed Ledger Technology

Distributed Ledger Technology (DLT)

When talking about cryptocurrencies the link is automatically made with blockchain technology, which is a distributed ledger technology (DLT). There are several of these. DLT is a decentralized, digital database. This means that the information within the database is not stored at one central point, but at several points simultaneously (decentralized) and that there is consensus about the data. This not only speeds up the provision of information, but also makes the system more difficult to manipulate. All information is given a time stamp and digital fingerprint (a 'hash') to prevent the data/information from being changed in the meantime.

DLT: advantages and disadvantages

The advantage of the DLT is that it can lead to efficiency gains in data exchange. Information becomes available more quickly and a single decentralised infrastructure is used in which all the information can be verified using the digital fingerprint. This eliminates the need for a third party or intermediary; everyone looks at the same data and the status of the data is no longer unclear. This not only saves time and money, but also optimises processes. The DLT can also add digital rights to an object or property (asset) or create smart contracts. These may, for example, be contracts about the periodic payment of dividends.

The system also has disadvantages, of course. A decentralised system, for example, automatically involves less supervision and control because certain parties fall by the wayside. This is a risk if the system is not set up properly. Security is another aspect: not only of the technology or the system, but also of the cooperation and/or agreements included in smart contracts, for example. Control and supervision are therefore necessary and will lead to greater trust and further integration of the technology.

Productivity improvement: DLT creates economic value

The elimination of intermediaries and the productivity improvement that DLT offers creates economic value. It can even be compared to the emergence of the Internet. The economic value of the Internet also mainly lies in the disappearance of many intermediaries, but then outside financial services. Consumption and production have been optimized, travel agencies have virtually disappeared and the space devoted to physical stores is decreasing because we order more online. As a result, less stock is held and price comparison has improved. The Internet makes all this possible and has made many services (intermediaries) superfluous.

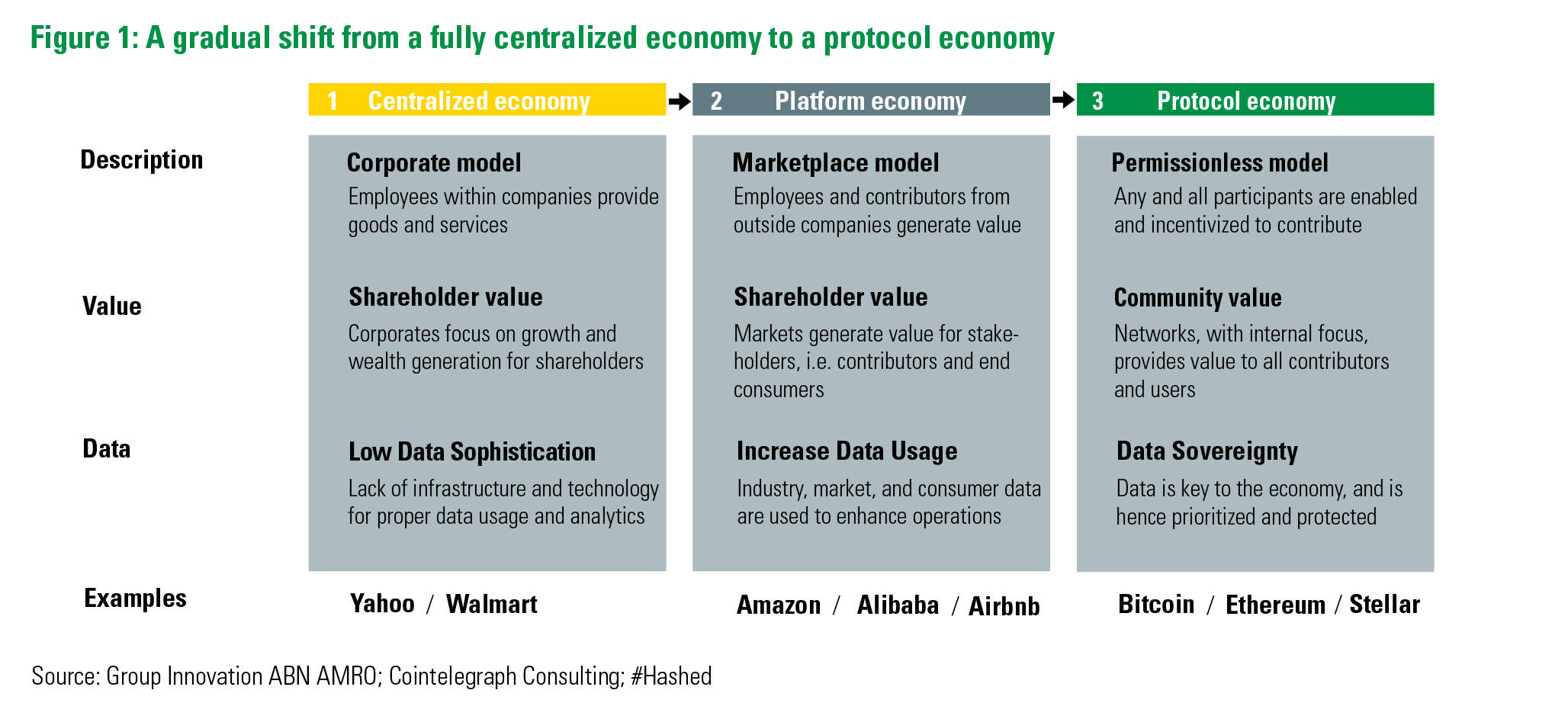

From centrally planned economy to protocol economy

Whereas the economic impact of the Internet lies mainly with consumer goods and services, DLT can do this for financial services, among others. If information about assets is easily accessible and is stored decentrally and safely, here too certain services will disappear, for example those of brokers, notaries, accountants, lawyers and bankers.

ABN AMRO believes that developments on the internet have resulted in a steady shift from a centrally planned economy, where little use was made of data, to a platform economy where the use of data has increased significantly. We estimate that with the rise of DLT this will gradually shift further towards a protocol economy, in which data is key to the economy. Data is thus prioritized and protected. The focus of the protocol economy is on building networks and limiting intermediaries (see Figure 1).

The economic value of tokenisation

Tokenisation: the creation of a digital certificate

As described above, distributed ledger technology makes it possible to assign rights digitally. The creation of such a digital certificate is called tokenisation. Tokenisation can apply to both physical and virtual goods. Examples are commodities, such as coffee or diamonds; consumer goods such as cars, art, smartphones or luxury handbags; financial instruments such as shares, bonds and real estate; but also legal matters such as patents, intellectual capital or forms of money such as savings programmes, fiat money (such as euros and dollars) or cryptocurrencies.

ABN AMRO anticipates further efficiency gains from tokenisation

Tokenisation offers opportunities for further efficiency gains. Liquid and illiquid assets can be split up into smaller parts. This also makes it easier to raise money or financing, for example, or to trade in it. It is also possible to make everything very transparent, with everyone having access to the information. Also, tokens are digital and accessible at any moment of the day, all year round. This makes it quicker and the function of the intermediary often falls away here too.

A condition is that the creation of such a digital certificate is transparent and is checked. The system only works if the input is also reliable and of high quality. The tokenisation of, for example, a painting by Van Gogh only works if the very first input actually concerns a Van Gogh and not a forgery.

The economic value of digital currencies

Finally, we discuss digital currencies, such as stablecoins and digital coins of central banks (CBDC, Central Bank Digital Currency).

Stablecoins provide liquidity

Stablecoins are a form of cryptocurrencies that have collateral and are linked (pegged). This collateral can consist of traditional assets such as currencies, commodities or real estate. It can also be digital assets, such as Ethereum or other crypto currencies. Stablecoins provide liquidity to the crypto market. Per stablecoin, a fixed unit of collateral is held, for example one dollar for every stablecoin issued. The most well known stablecoin is USD Tether. Despite the considerable value of Tether, there are serious questions as to whether Tether holds sufficient collateral. For this it has to answer in court. This shows that stablecoins need more supervision, partly because the user of the stablecoin runs the risk if the issuer of the stablecoin is not reliable. Therefore, there are even calls for stablecoins to be supervised by banks.

Many central banks are investigating CBDCs

Central banks are also exploring digital currencies. A full 70% of central banks indicate that they are investigating or will investigate CBDCs. China and Sweden are in the lead, while the ECB is also investigating a digital euro. An essential difference with cryptocurrencies is that CBDCs are issued from a centrally managed system, with the central bank as issuer: in other words, an issuer with low risk.

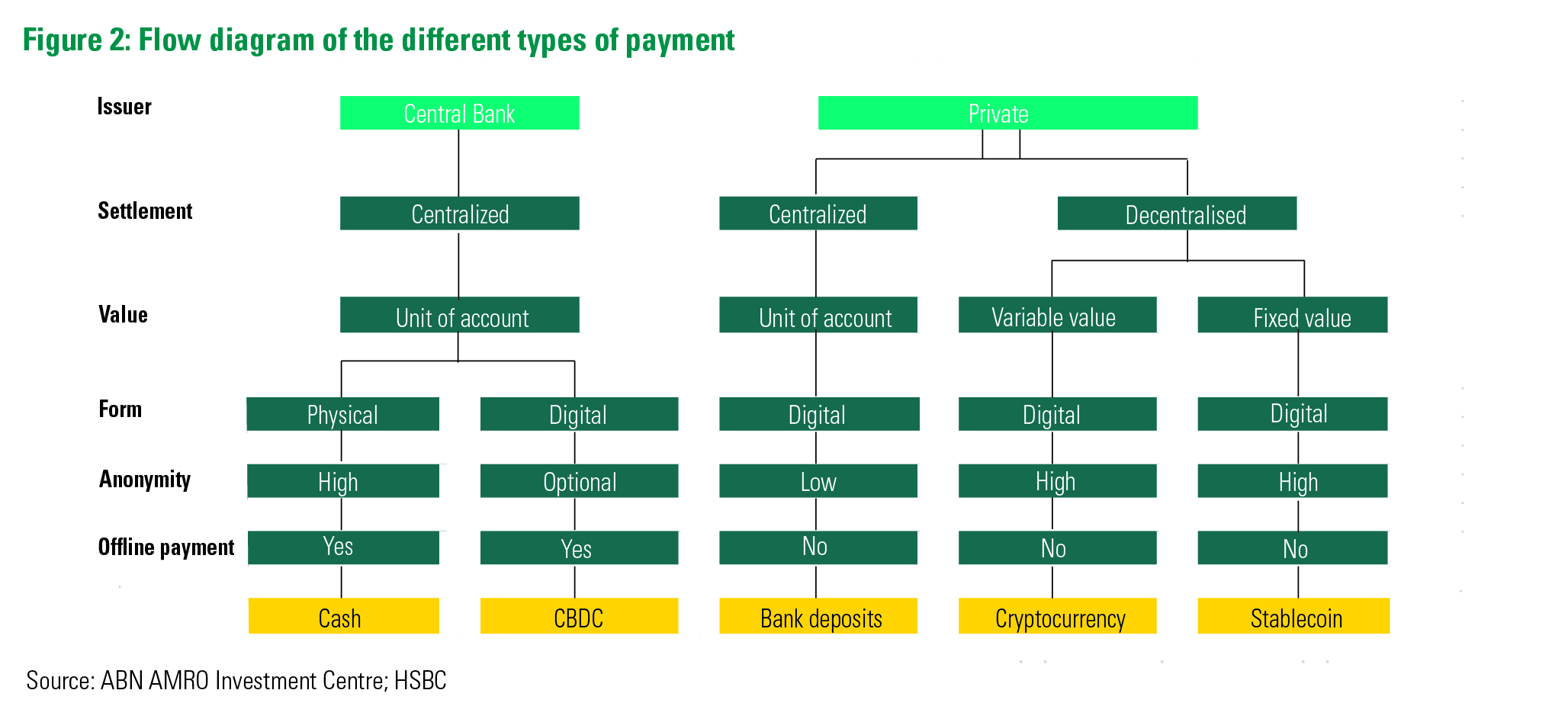

One of the reasons that central banks are investigating this is because pressure is growing to speed up the normal payment process and make it more accessible and efficient. International money transfers take a lot of time, are expensive and inefficient. This is because money has to be transferred internationally through correspondent banks, often in a different currency from that of the originator. Crypto currencies do not have this problem, because they use a decentralised database which is accessible 24 hours a day. The development of digital currencies is therefore a potential threat to financial parties involved in payment transactions (think of parties such as Visa, Mastercard, PayPal, Western Union, but also ABN AMRO). For an overview of the different payment methods, see Figure 2.

ABN AMRO expects increased prosperity due to digital money

Once regulated, stablecoins or CBDCs manage to form a reliable payment system, they can offer some great benefits. For example, it provides users with access to money, and thus the ability to save, invest, borrow and/or finance. Many people and small businesses, especially in developing countries, do not have access to this (see Figure 3), while this access can lead to productivity gains and thus economic growth. As a result, the level of prosperity in these countries can improve.

It is also being investigated how digital money can be made programmable. This makes it possible to use it in a very targeted way. For example, a government subsidy for housing or study can be paid through a CBDC. In that case, the CBDC is programmed to serve only the purpose of paying rent or tuition fees. A time limit can also be given in which the subsidy must be spent. If this is not done, the money loses its value for the user. Digital money is also a solution in view of the further rollout of the Internet of Things (IoT), where robots or smart devices increasingly communicate with each other. They can use digital money to pay each other for services rendered, without interference from humans.

In short: Digitisation of the financial industry can lead to a protocol economy and increased prosperity

Conclusion triptych cryptocurrencies

As described in part one of this three-part series, ABN AMRO does not currently advise or invest in cryptocurrencies because of the high risk, the difficult valuation issue and the lack of regulation. Even though regulation will wipe out part of the efficiency gains, regulation is essential to achieve further integration of the technology. A future investment case will then be based on the technological development and use case (function) of a cryptocurrency.

To have exposure to this promising technological development, investors can look to companies that are enabling this technological development. These can be technology companies or fintechs, and also existing financial institutions that are working to make the transition.

Ralph Wessels

Head of Investment Strategy at ABN AMRO

- Tokenization of Assets, Nov. 2020 -

- Announcing Strike Global, Jan. 2021 - Jack Mallers' blog

- Cryptoassets: The guide to Bitcoin, Blockchain, and Cryptocurrency for investment professionals, Jan. 2021 - CFA

- Our Thoughts on Bitcoin, Jan. 2021 - Bridgewater

- The rise of Bitcoin, Jan 2021 - UBS

- Bitcoin: A Solution In Search Of A Problem, Feb. 2021 - BCA Research

- Bitcoin, Gold, Or Fiat, Feb. 2021 - Evergreen Gavekal

- The 2021 Crypto Crime Report, Feb. 2021 - Chainalysis

- Bitcoin At the Tipping Point, Mar. 2021 - Citi

- The Bitcoin Experiment, Mar. 2021 - Neuberger Berman

- Understanding Bitcoin, Mar 2021 - Fidelity

- The Case for Cryptocurrency As an Investable Asset Class in a Diversified Portfolio, Mar. 2021 - Morgan Stanley

- Digital currencies: What are they and why do they matter, Mar 2021 - HSBC

- The future of Bitcoin, Apr. 2021 - Rabobank

- Why Cryptocurrencies Are Here To Stay, Apr. 2021 - BCA Research

- Bitcoin as digital gold - a multi-asset perspective, Apr. 2021 - Robeco

- How To Short Bitcoin, Or Anything Else, Without Losing Your Shorts, Apr. 2021 - BCA Research

- Bitcon No More, Apr. 2021 - Evergreen Gavekal

- Covcoins: The digital currencies that matter, May 2021 - The Economist

- How fintech will eat into banks' business, May 2021 - The Economist

- When central banks issue digital money, May 2021 - The Economist

- The Crypto Impossibility Theorem, May 2021 - BCA

- Buy The Crypto Dip, May 2021 - Gavekal Research

- Bit by bit, May 2021 - The Economist

- The rise of crypto laundries: how criminals cash out of bitcoin, May 2021 - Financial Times

- Who's Who on the Blockchain, June 2021 - Chainalysis

- The Future of payments: programmable payments in the IoT sector, June 2021 - CashOnLedger; Digital Euro Association, Frankfurt School Blockchain Center; PPI

- Cryptos' Many Damocles' Swords, July 2021 - Evergreen Gavekal

- Deep in rural China, bitcoin miners are packing up, July 2021 - The Economist

- The Tether Discussion, July 2021 - The Grant Williams Podcast

- Cryptocurrency Valuation and Network Size, July 2021 - Goldman Sachs

- DeFi paradoxes, July 2021 - Financial Times

- Cryptocurrencies and ESG, July 2021 - Candriam

- Untethered, July 2021 - Evergreen Gavekal

- Why regulators should treat stablecoins like banks, Aug. 2021 - The Economist

- Cryptocurrency Market Segments, Aug. 2021 - Goldman Sachs

- Why Investors Cannot Ignore Bitcoin Any More, Aug. '21 - Evergreen Gavekal

- Cryptocurrencies: developing countries provide fertile ground, Sept. '21 - Financial Times

- Adventures in DeFi-land, Sept. 2021 - The Economist

- Just add crypto, Sept. 2021 - The Economist