Cryptocurrencies part 2: Bitcoin

Bitcoin evokes emotion

Clear use case: condition for success

Since Bitcoin's inception at the end of the financial crisis, 18.6 million Bitcoins have been mined (for more on mining, see our 2018 report). It will take approximately until 2140 before all 21 million Bitcoins are mined. Whether Bitcoin will finally catch on is still unclear. What we do think is that the longer Bitcoin exists, the more likely it is that the coin will be here to stay. It helps that Bitcoin's underlying technology (the blockchain) is conceptually simple. Bitcoin is also credited with the benefits of the network effect. The network effect means that more users strengthen a network. This in turn attracts new users, which makes the network even stronger, et cetera, et cetera. The network effect increases the likelihood that Bitcoin will continue to exist if it has a clear use case that adds value. Otherwise, given the low barriers to entry and the possibility of alternatives, there is a real chance that this crypto coin will be a temporary phenomenon.

Bitcoin as a means of payment, an investment or neither?

Bitcoin as a means of payment

Some advantage in large international Bitcoin transactions (+)

The great advantage of Bitcoin is that it can be paid and settled instantly from a reliable network at any time of the day, all year round. This can be especially beneficial for large international transactions, as it saves time on processing.

Paying with Bitcoin is inefficient in several ways (-)

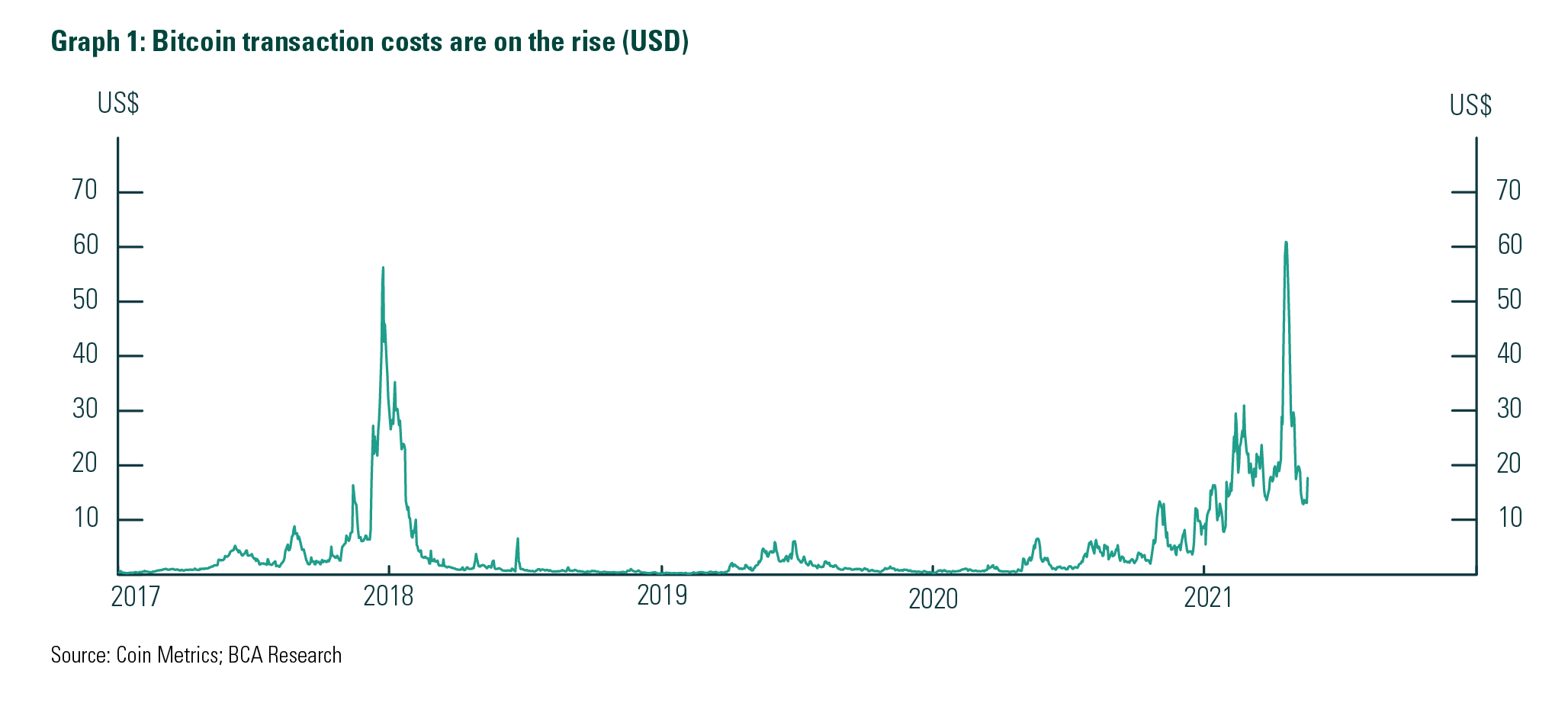

In general, however, Bitcoin is inefficient as a means of payment in several ways compared to the current fiat money system (euros, dollars, etc.). For example, for the vast majority of payments, transaction costs are too high, a normal transaction takes longer than, say, a domestic payment, a transaction (or mining a block) costs a lot of electricity, the number of transactions is limited, and the fact that prices are not displayed in Bitcoins means that conversion to and from fiat money is required. In addition, costs and waiting time increase when the network becomes busier (Graph 1). These inefficiencies are one of the reasons why the use of Bitcoin as a payment method has not yet taken off (Graph 2). The 'lightning network' that is being developed tries to solve some of these inefficiencies (speed and cost).

Decentralised system undermines sovereignty (-)

What is underestimated is that a global decentralised money system erodes the sovereignty of countries. A central system with its own currency enables governments and central banks to stimulate, tax, sanction and/or control malicious money flows. Therefore, a decentralised system is not in the public interest and governments will stick to their own currencies. As a result, businesses and consumers using Bitcoin will have to keep converting between the local currency and Bitcoin. This is inefficient.

Bad experiences with rigid and decentralised money system (-)

Despite the fact that the limited number of Bitcoins is seen as an advantage, for a widely used currency it is actually a major disadvantage. The abandonment of the gold standard was partly due to the rigidity of that system. Less fiscal and monetary stimulus made recessions more frequent. The same applies to a decentralised banking or money system. In the past, this led to a banking crisis more often than a centrally managed system. Ultimately, a rigid and decentralised money system is at the expense of prosperity. For example, after the corona outbreak and the subsequent lockdowns, the world economy would have fallen into a deep depression if stimulus measures had been severely limited by a rigid monetary system.

Stable price level essential for confidence (-)

Finally, it is essential that a currency has a stable price level. This creates trust and is therefore often one of the most important tasks of a central bank. Unfortunately, for Bitcoin this is anything but the case. Price stability is achieved when (the growth of) demand is in line with (the growth of) supply. Because the supply of Bitcoins is limited and the growth of the number of Bitcoins is decreasing, the usage (demand) will have to decrease in order for the price to become more stable. Due to these limitations and the low barriers to entry, the likelihood of other digital payment alternatives is real.

Table 1: Pros and cons of Bitcoin as a payment method

Advantages (+) | Disadvantages (-) |

- Worldwide payment and settlement 24/7/365 | - Bitcoin is inefficient as a means of payment: |

- Decentralised system | - Bitcoin cannot be decentralised, correct and time & cost efficient at the same time |

- More and more businesses explore the possibility of Bitcoin payments | - The limited number of Bitcoins is a major drawback for serving as a (global) means of payment |

- Large (international) amounts in Bitcoin are more efficient | - Own currency and central bank gives a country or monetary union sovereignty and freedom of movement |

- Bitcoin can work as an alternative in countries where there is little confidence in the currency, government, or where hyperinflation is occurring or normal money transactions are being banned; these are the exceptions worldwide. | - List of countries banning Bitcoin is getting longer; however, a decentralised system is impossible to ban completely; it may, however, slow down its development and use, leading to lower acceptance and reducing its network effect |

- Stable price level is essential for trust; Bitcoin is extremely volatile which lowers user adoption | |

| - Price volatility is low when demand growth is in line with supply growth; Bitcoin growth continues to decline, which should lead to lower usage to achieve price stability |

| - Until 2140, the Bitcoin blockchain will be protected and maintained by miners; reward is currently 6.25 Bitcoin for an approved block (will be 0.2 in 2040 and from 2140 onwards, users will bear all costs) |

| - Risks: |

Bitcoin as an investment

Bitcoin not to be valued as a stock

In addition to being a means of payment, Bitcoin is increasingly being mentioned as a potential investment or asset class. What matters here is if Bitcoin can be valued. Since Bitcoin does not generate cash flow like a stock does in the form of dividends, it cannot be valued using a discounted cash flow model (one of the ways to value stocks). Therefore, it has been suggested that Bitcoin should be seen more as a commodity, currency or collectible because of its similarities to these asset classes. Commodities, currencies and collectibles are priced rather than valued. The price is based on supply and demand and on economic value. However, gold, precious stones, land, wine, art, etc. all have one or more functions (Graph 3). That makes them consumer goods as well as a medium of exchange. Bitcoin is not.

Crypto valuation methods

In theory, there are several valuation methods, which research institute CFA also describes in its report, some of which are mentioned here. None of these methods are perfect or ideal for valuing cryptos. However, it is interesting to briefly explain them, as they provide some insight.

Total Addressable Market

The first method is the total addressable market method or TAM. This looks at the market of which a product, or in this case the crypto, is part and of which it is known how much it is worth. The value is then determined by looking at what market share the product is able to capture in that market.

Equation of Exchange

The second method is the Equation of Exchange by Chris Burniske. This method looks at the valuation of money. Money can be valued according to the following equation MV = PQ. Here M is the total money supply. This is multiplied by the velocity of money (V). This is equal to the price (P) multiplied by the quantity (Q). In crypto currencies, M would stand for the market capitalisation of the token, V for the turnover rate, P for the price and Q for the number of transactions.

Metcalfe's Law

The valuation method of Metcalfe's Law is used to value networks, such as social media networks. The calculation is quite simple by taking the number of users squared. The idea here is that the more people participate in the network, the stronger the network becomes and the more the network becomes worth. This applies to both monetary value and utility for the user.

Cost of Production and Stock-to-Flow

Adam Hayes developed the Cost of Production valuation. This method looks at what it costs to mine a crypto. The last valuation method is called Stock-to-Flow. This method is often used with natural resources. It looks at the ratio of the amount that is currently available to the amount that is added each year. For Bitcoin, this method mainly expresses scarcity because there are fewer of them each year.

Bitcoin seen as a rival to gold (+)

More and more financial institutions are offering financial instruments to invest in Bitcoin and other crypto currencies. As a result, Bitcoin is becoming more mainstream. Bitcoin is mainly seen as digital gold with a store of value. According to this idea, Bitcoin would be a good alternative to gold because the coin is even scarcer.

Demand for anti-fiat money increases (+)

As long as there are groups in society that do not trust institutions and the current monetary system, there will be a demand for anti-fiat money. This demand has increased since the banking crisis and the corona crisis as a result of the low interest rate policies and the buy-back programmes of central banks. Currently, gold, among other things, fulfils the role of anti-fiat money. Some see that Bitcoin, because of its scarcity, could also partly take on this role.

Valuation and portfolio added-value are difficult to establish (-)

Bitcoin remains difficult to value because it is still not clear what purpose the token serves. This makes investing difficult. Also, part 1 of our crypto-triptych has already shown that research does not unequivocally prove that Bitcoin provides diversification and low correlation in an investment portfolio (Graph 5). Despite summary research showing that the investor is compensated for the risk taken, the difference is small and no tactical advice can be given. The latter suggests that a price movement can be poorly estimated. Investing in Bitcoin therefore remains a black box.

Comparison with gold is flawed (-)

Furthermore, the comparison between Bitcoin and gold is flawed in several ways. Central banks still hold a lot of gold reserves. Confidence in gold is also reflected in its various functions (see Graph 3). This is not the case with Bitcoin. In addition, Bitcoin is very volatile. Price fluctuations of 20% are very frequent, while Bitcoin has lost 80% of its value three times in its still short existence since 2010. Graph 4 shows this from 2013 onwards. The hallmark of a store of value is protection against loss. With Bitcoin, this is not the case and price movements are more indicative of speculation. This is also warned against, leaving Bitcoin at risk of regulators or governments banning the digital currency as an investment.

Bitcoin not interesting for ESG investors (-)

Bitcoin is not sustainable. For many investors, that argues against the currency. This is all the more true as investing according to ESG (environmental, social and governance) criteria is becoming more common. Not only does the Bitcoin network consume more electricity than, say, the Netherlands, Argentina, or Norway, but Bitcoin also reinforces inequality. A relatively small group of people have a very large stake in all Bitcoins (Graph 6). This, in turn, goes against the original idea that Bitcoin was supposed to be for everyone.

Table 2: Pros and cons of Bitcoin as an investment

Advantages (+) | Disadvantages (-) |

- Momentum for Bitcoin is increasing with more and more financial parties offering crypto services. Each step leads to further professionalisation with the crypto world becoming more mainstream. | - Bitcoin has a market value, but no intrinsic or economic value and is difficult to value despite different methods. Lack of a clear use case makes an investment difficult, as understanding what you are investing in is a basic principle. |

- In theory, Bitcoin should provide low correlation and diversification in an investment portfolio (the reality is different). | - Bitcoin has been compared to gold, gems, land, and collectibles like wine and art. All of these things have no cash flow but still have one or more functions. Also, in addition to being a means of exchange, they are consumer goods, which Bitcoin is not. |

- Bitcoin is affectionately known as 'digital gold' and seen as a store of value. The limit on the number of Bitcoins makes the coin scarcer than gold, as gold continues to be found. The negative (real) interest rates also speak in favour of Bitcoin and gold. | - The gold equation is flawed on several counts. The gold standard has been abolished, but central banks still hold gold reserves, so an indirect link remains. It is from this that gold derives part of its investment value. This link and the trust are both missing with Bitcoin. |

- As long as there is fiat money and a section of society distrusts official institutions including central banks, there will be a demand for 'anti-fiat money'. Anti-fiat money is seen as a protection against the depreciation of the fiat money system. | - In its short history, Bitcoin has been both a risk-on and risk-off asset. This makes the coin difficult to qualify for an investment portfolio. The claim that Bitcoin is digital gold and a store of value is therefore unfounded. This is clearly reflected in the volatile price curve. |

- The high energy consumption of the Bitcoin network need not, in essence, be an argument against investing. Mining gold or other raw materials is not environmentally friendly either, but it is meeting with increasing resistance. | - Bitcoin, like gold, is seen as a protection (hedge) against the devaluation of current money. However, equities have proven to be a better inflation hedge, partly because of their cash flow. Gold has only been a better hedge in times of hyperinflation. |

| - Part 1 of our three-part series shows that there is no single conclusion that Bitcoin provides diversification and low correlation in an investment portfolio. |

| - The price of Bitcoin is very volatile and it is difficult to estimate a price movement. Therefore, it remains a black box and tactical allocation is difficult. |

| - The enormous volatility also shows that liquidity in the market is still a problem. This will make (institutional) investors cautious. |

| - Due to its enormous volatility and speculative nature, which even professional parties warn their clients about, Bitcoin remains at risk of being banned from investment by regulators or governments. |

| - It is striking that the enthusiasm for Bitcoin and crypto is largely retail-driven. Without many people being able to specify exactly what they are 'investing' in, the hope of high returns seems to prevail. The offer of crypto services is also very much driven by customer demand. Financial institutions with knowledge of the monetary system and financial markets remain reluctant to embrace Bitcoin and warn against speculation. |

| - The extreme energy consumption and uneven distribution of Bitcoins increases inequality, which will deter ESG investors. |

To sum up: Bitcoin is unsuitable as a means of payment and highly speculative as an investment

ABN AMRO does not give advice on crypto currencies and therefore not on Bitcoin. Furthermore, most arguments speak against Bitcoin as a means of payment. Bitcoin is not efficient, and its limited number is a major limitation. Generally speaking, something is successful when everyone adopts it en masse. This happens naturally when things become more efficient or add value for the user. Since neither seems to be the case for Bitcoin, this will weaken its acceptance. This, in turn, will weaken the network effect and make it harder for Bitcoin to become a global currency.

Cryptos and Bitcoin as an investment are undergoing a professionalisation process. More and more financial service providers are offering the opportunity to invest in them. In addition, Bitcoin is scarcer than gold and could partially take over gold's function as an anti-fiat money. This could put a floor under the price of Bitcoin if people are willing to pay an ever-higher price. Fundamentally, however, it is difficult to make a case for Bitcoin. The digital currency has no intrinsic or economic value. In addition, research has shown that it is questionable whether Bitcoin belongs in an investment portfolio at all (see part 1 of this three-part article) and that comparisons with gold are flawed. On balance, Bitcoin is not a store of value, but rather a speculative investment. Finally, the Bitcoin network consumes a lot of electricity and increases inequality. As such, it does not meet sustainable investment criteria (ESG).

Ralph Wessels

Chief Investment Strategist ABN AMRO

Sources:

- Tokenization of Assets, Nov. 2020 – EY

- Cryptoassets: The guide to Bitcoin, Blockchain, and Cryptocurrency for investment professionals, Jan. 2021 – CFA

- Our Thoughts on Bitcoin, Jan. 2021 – Bridgewater

- The rise of Bitcoin, Jan. 2021 – UBS

- Bitcoin: A Solution In Search Of A Problem, Feb. 2021 – BCA Research

- Bitcoin, Gold, Or Fiat?, Feb. 2021 – Evergreen Gavekal

- The 2021 Crypto Crime Report, Feb. 2021 - Chainalysis

- Bitcoin At the Tipping Point, Mar. 2021 – Citi

- The Bitcoin Experiment, Mar. 2021 – Neuberger Berman

- Understanding Bitcoin, Mar. 2021 – Fidelity

- The Case for Cryptocurrency As an Investable Asset Class in a Diversified Portfolio, Mar. 2021 – Morgan Stanley

- Digital currencies: What are they and why do they matter, Mar. 2021 – HSBC

- The Future of Bitcoin, Apr. 2021 - Rabobank

- Why Crypto’s Are Here To Stay, Apr. 2021 – BCA Research

- Bitcoin as digital gold – a multi-asset perspective, Apr. 2021 – Robeco

- How To Short Bitcoin, Or Anything Else, Without Losing Your Shorts, Apr. 2021 – BCA Research

- Bitcon No More, Apr. 2021 – Evergreen Gavekal

- Covcoins: The digital currencies that matter, May 2021 – The Economist

- How fintech will eat into banks’ business, May 2021 – The Economist

- When central banks issue digital money, May 2021 – The Economist

- The Crypto Impossibility Theorem, May 2021 – BCA

- Buy The Crypto Dip?, May 2021 – Gavekal Research

- Bit by bit, May 2021 – The Economist

- The rise of crypto laundries: how criminals cash out of bitcoin, May 2021 – Financial Times

- Who’s Who on the Blockchain, June 2021 - Chainalysis

- Cryptos’ Many Damocles’ Swords, July 2021 – Evergreen Gavekal

- Deep in rural China, bitcoin miners are packing up, July 2021 – The Economist

- Cryptocurrency Valuation and Network Size, July 2021 – Goldman Sachs

- Crypto’s and ESG, July 2021 – Candriam