Calculation example: Vincent and Isabelle

When can they stop working?

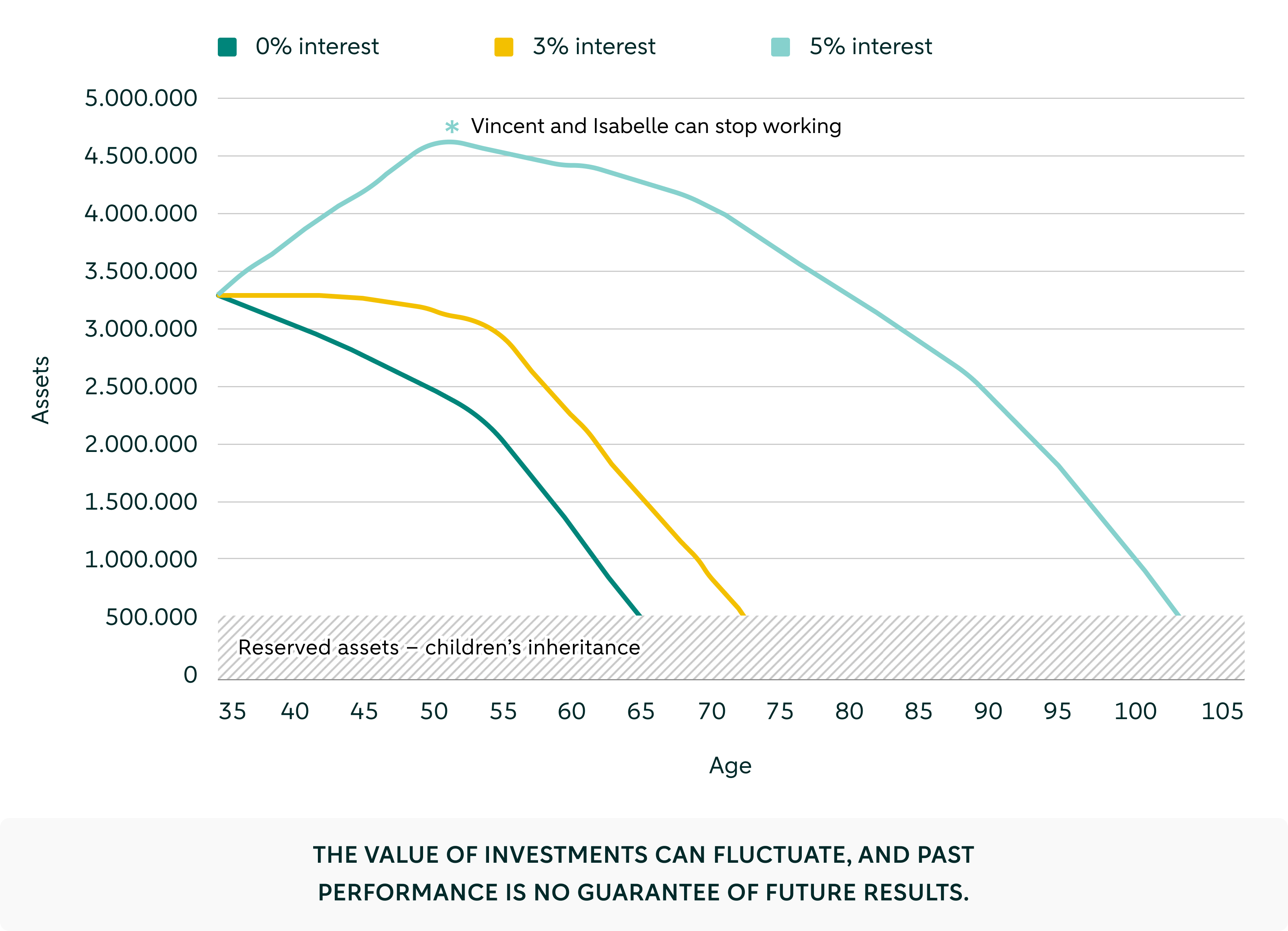

Vincent received €3.3 million for his share in an IT company. With a return of 5%, he and Isabelle can stop working earlier. They can live comfortably and leave their children a substantial inheritance.

Investing can be attractive, but it involves risks. You may lose (part of) your investment.

Vincent (35) is a programmer and lives with Isabelle (32) and their two children. He received €3,300,000 privately for his shares in the IT company where he worked, after it was sold. He received these shares as part of his remuneration when he joined the company a few years ago as a senior programmer. At that time, the company was still a start-up.

Vincent does not see himself as a true entrepreneur and therefore accepted a position as a programmer at a large company. His salary is €80,000 gross per year, all-in. Isabelle works part-time and earns €30,000 gross per year. Last year, Vincent bought an apartment for €500,000, which he financed entirely with an annuity mortgage at an interest rate of 2%.

Vincent wants to grow his wealth so that he and Isabelle can stop working earlier. They want to work for no more than another 20 years. Each year, they want to be able to spend €80,000 net, with their spending power keeping pace with inflation of 2% per year. This means that annual spending power should, for example, be just over €97,000 after 10 years and almost €119,000 after 20 years. Vincent also wants to leave at least €250,000 to each child.

Scenario: 0% investment return

Vincent wants to grow his wealth. With an investment return of 0%, however, the impact of inflation and taxes becomes clearly visible. In this case, Vincent and Isabelle can maintain their desired lifestyle until they are 65 and 62 respectively. They can leave €250,000 to each child and will then only own their home, which will have been fully repaid.

Scenario: 3% investment return

With a conservative investment return of 3% per year, the wealth grows noticeably, as Vincent had hoped. In this scenario, Vincent and Isabelle’s money only runs out when they are 73 and 70 years old. They can leave €250,000 to each child and will then only own their fully repaid home.

Scenario: 5% investment return

With an investment return of 5% per year, Vincent’s wealth grows sufficiently for them to stop working after 20 years. The wealth only runs out when Vincent is 103 and Isabelle is 100. They can each leave their children at least €250,000 and will then only own their fully repaid home.

Your wishes and goals

The example above shows how different return scenarios can affect your financial future. As a committed Private Bank, we understand that your wishes and goals are unique and that your situation calls for a tailored approach. Together, we explore various financial scenarios. Read more about Wealth Planning or make an appointment.

Investing involves risks

You should only invest money that you can spare, in addition to keeping a buffer for unexpected expenses. Investing can be appealing, but it does come with risks. You may lose (part of) your deposit. It is important to be aware of this.

Contact

Interested in private banking?

Would you like to get to know us with no obligation and discuss your wishes and goals?

Schedule a meeting directly. We are looking forward to meeting you.

For clients

Do you have a question about your daily banking matters? Please contact Private Assistance:

+31 (0)20 343 43 43 | Wk 8.00am-9.00pm - Sa 9.00am-5.30pm

Would you like to get in touch with your private banker? You'll find their current contact details in your Internet Banking.

Interested in private banking?

Would you like to get to know us with no obligation and discuss your wishes and goals?

Schedule a meeting directly. We are looking forward to meeting you.

For clients

Do you have a question about your daily banking matters? Please contact Private Assistance:

+31 (0)20 343 43 43 | Wk 8.00am-9.00pm - Sa 9.00am-5.30pm

Would you like to get in touch with your private banker? You'll find their current contact details in your Internet Banking.